Deep dive into Brazil’s latest Open Finance Report: From Regulation to Global Benchmark

Brazil’s Open Finance is one of the world’s most ambitious financial ecosystem initiatives. In this blog article, we explore the country’s most recent annual report, published in July 2025, which examines key developments and insights through a series of critical questions.

Open Finance in Brazil

This initiative, launched in 2020, allows authorized participants (i.e., from banks and FinTechs to insurers and payment providers) to share data securely, promoting inclusion, enhancing offerings, and fostering competition. It was implemented by the Central Bank of Brazil (Banco Central do Brasil, BCB) which still remains the main regulator, setting rules, standards, API specifications, security protocols, and consent frameworks, while monitoring compliance and ensuring alignment with broader financial stability goals. Although this Open Finance program is centrally regulated, APIs are developed and deployed individually by institutions, combining standardization with operational flexibility.

How is Brazil’s Open Finance funded and supported?

Brazil’s Open Finance is primarily supported through a combination of regulatory oversight and institutional investment. BCB has played a central role, providing strategic guidance, regulatory oversight, and initial funding to develop foundational infrastructure and technology. With Resolution BCB 400, published on July 4, 2024, the Central Bank established a formal governance structure responsible for strategic definition, operational management, and supervision of the system, ensuring regulatory compliance and alignment with best practices.

The model also promotes the ecosystem’s financial sustainability through shared funding by participating banks, Fintechs, insurers, and payment providers, who invest in building and maintaining APIs and data infrastructure, while the Open Finance Governance Entity coordinates standards and best practices to support smooth operation and long-term growth.

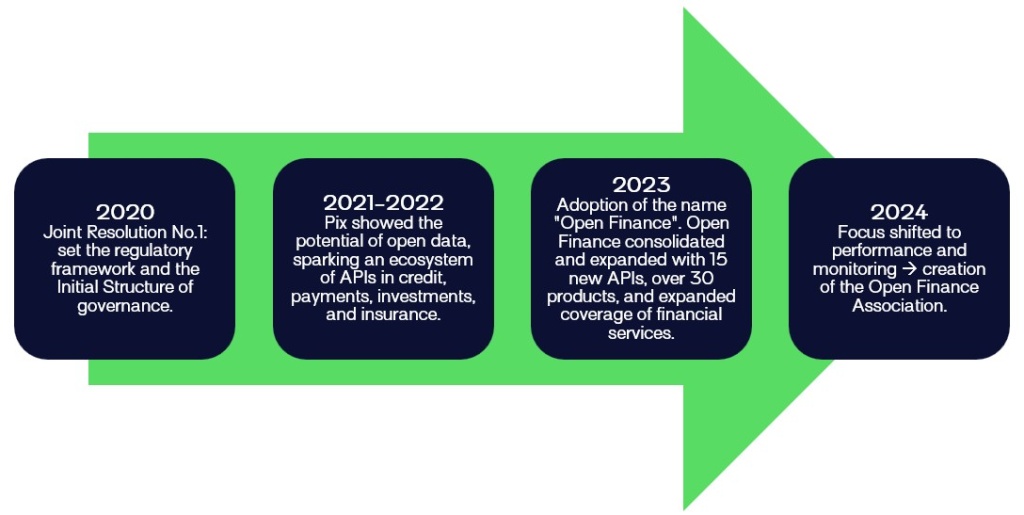

How has Brazil’s Open Finance been developed throughout the years?

The establishment of the Open Finance Association (OFA), in 2024, marked a turning point by formalizing collaboration between the regulator and industry participants. This co-governance structure reflects a broader global trend: combining strong oversight with industry expertise to balance innovation, compliance, and stability.

As highlighted in Report, this evolution (from regulatory pilots to structured co-governance) has been critical in guiding investments, strengthening API performance, and sustaining ecosystem growth. Together, these factors have positioned Brazil as a global reference point for resilient and scalable open finance systems.

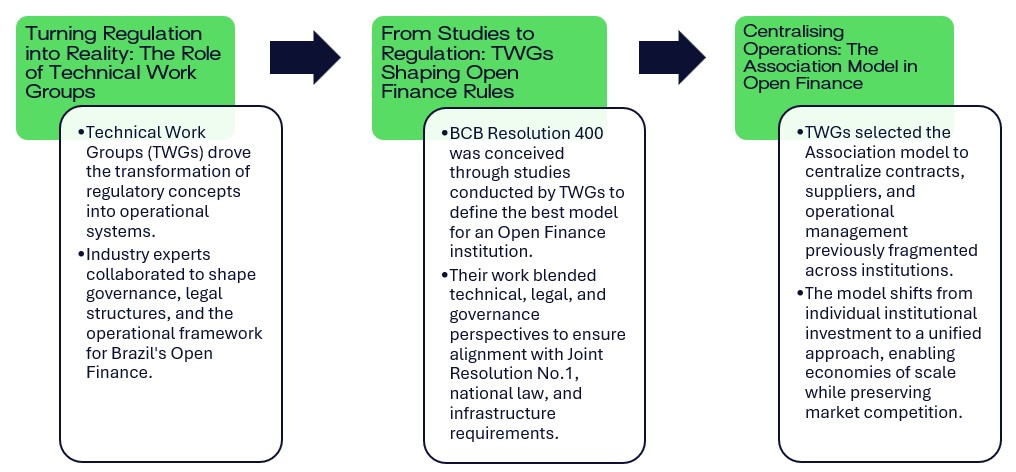

The Technical Foundation: How Industry Expertise Shaped Modern Governance?

What is the Open Finance Association and why was it created?

- Constitutional milestone: Officially established on 27 December 2024, formalizing the collaborative industry structure into a legally constituted entity responsible for coordinating and supporting the Open Finance ecosystem in Brazil.

- Governance transition: Serves as a coordination and governance body for the ecosystem, complementing but not replacing BCB’s regulatory authority.

- Legal structure: Operates as a non-profit entity comprising banks, Fintechs, insurers, and payment providers, collectively guiding ecosystem development and strategy. It is headquartered in São Paulo with national reach and indefinite duration, operating under civil law and specialized bylaws.

- Infrastructure role: Collaborates with technology partners to support the infrastructure needed for secure, standardized API data sharing, but does not manage or regulate the API platform; that is BCB’s responsibility. Although the day-to-day management and technical operation of the APIs are handled by the individual participating institutions, as mentioned earlier.

- Long-term sustainability: Promotes financial sustainability through shared funding and collaborative governance among participating institutions.

- Global positioning: Positions Brazil’s Open Finance initiative to serve as a global reference point for resilient, scalable, and well-governed financial systems.

From Governance to Performance: Measuring the Impact of Institutional Evolution

With OAF now providing structured governance, the Report offers concrete evidence of how this institutional framework translates into operational success. The data reveals a maturing ecosystem where strategic investments, disciplined financial management, and improving technical performance demonstrate the real-world impact of Brazil’s governance evolution.

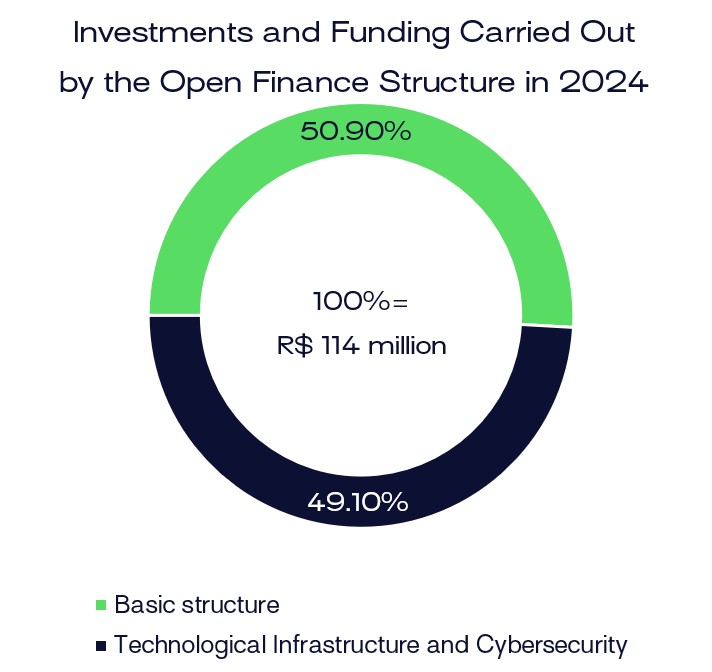

- Total investment: R$114 million in 2024 (≈ €18.247.182), a 20% increase from 2023.

- Basic structure:

- BCB provided initial funding to establish the Open Finance program, its governance framework, and the Open Finance Association Brazil for ecosystem coordination.

- Participating institutions fund the deployment, operation, and maintenance of their own APIs and internal systems.

- Shared funding ensures long-term sustainability, balancing investment in innovation, security, and governance across the ecosystem.

- Technological Infrastructure & Cybersecurity:

- Infrastructure: APIs, core IT systems, integration tools, and monitoring platforms.

- Cybersecurity: Encryption, authentication, audits, incident response, and staff training.

- Funding: Initial investment by BCB, ongoing contributions from banks, Fintechs, insurers, and payment providers.

- Balanced split: Nearly equal allocation between basic operational structure (50.9%) and technological infrastructure with cybersecurity (49.1%).

- Strategic rationale: Investments in infrastructure and cybersecurity help fix early gaps, ensuring smaller institutions can securely and reliably integrate with the ecosystem.

- Consumer impact: Loan applications process in minutes instead of days, consistent payment systems across banks and Fintechs, stronger fraud protection for shared financial data. Ultimately, consumers’ experience is faster, more reliable, and without compromising data security. Thereby building trust in digital financial services.

- Market positioning: Secure and efficient ecosystem attracts international investment and appeals to global FinTech companies entering emerging markets.

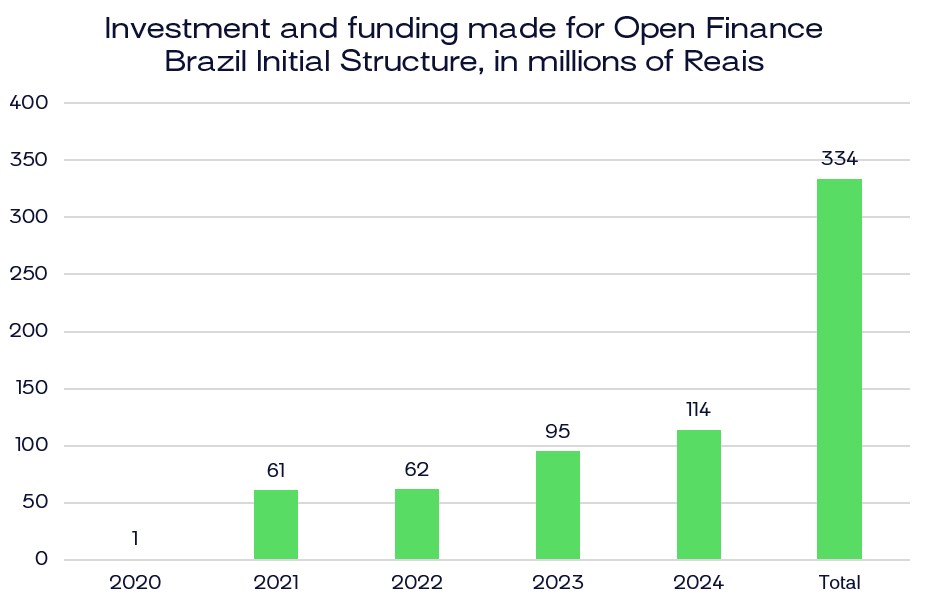

- Investment growth trajectory: Steady increase from R$1 million (2020) (≈ €160.100) to R$114 million (2024) (≈ €18.247.182), with total cumulative investment of R$333 million (≈ €53.313.300) over five years.

- Controlled spending approach: 2024 governance structure executed only 78% of approved budget, demonstrating disciplined financial management inherited from pre-Association regulatory bodies.

- Governance continuity: Financial discipline maintained by Deliberative Board and regulatory bodies established before the Association’s December 2024 creation.

- Multi-year spending pattern: Consistent controlled spending across multiple years reflects a systematic financial management approach rather than one-off restraint.

- Stakeholder benefits: Participating institutions gain confidence in efficient contribution management, regulators see sustainable long-term planning, consumers benefit from stability-focused system design.

- Strategic reserves: Underspending creates financial cushion to address unexpected technical challenges and support smaller institutions with integration difficulties.

- Quality over expansion: Financial approach prioritizes service stability and quality over rapid growth that could compromise system performance.

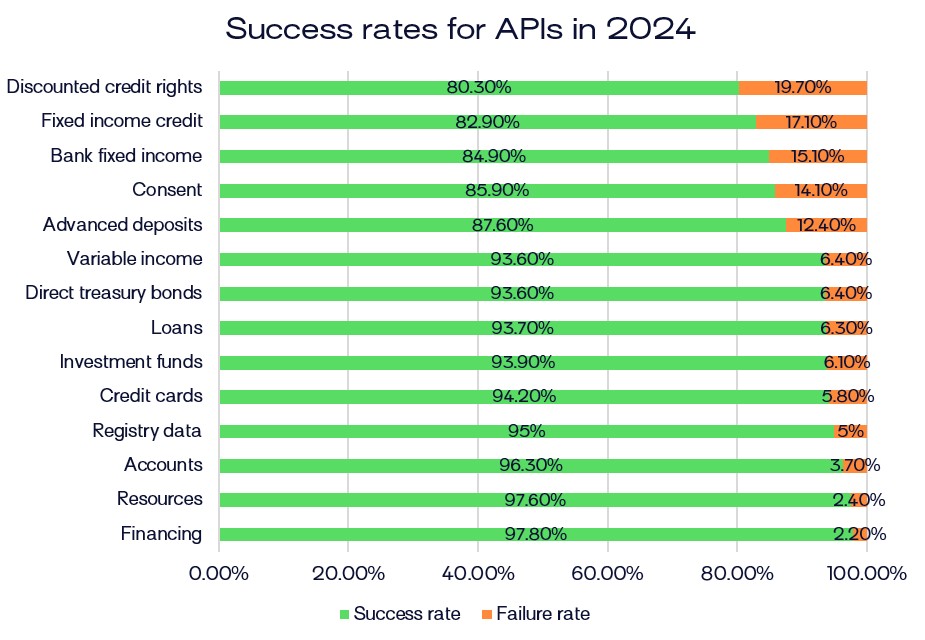

- Top performers: Financing (97.8%) and Resources (97.6%) APIs demonstrate nearly universal reliability, with 98 out of 100 user requests processed successfully.

- Strong core services: Accounts (96.3%), Registry data (95%), and Credit cards (94.2%) maintain high success rates for fundamental banking operations.

- Performance gaps: More complex services show lower success rates – Discounted Credit Rights (80.3%), Fixed Income Credit (82.9%), and Bank Fixed Income (84.9%).

- Technical readiness disparity: Success rate variations reflect differing levels of technical readiness among participating institutions rather than systemic failures.

- Governance impact: 2024 results reflect foundational work and governance structures established before the Association’s creation in December 2024.

- Customer experience: Core Open Finance services such as financing and resources, operate reliably under the BCB’s technical standards. In contrast, some specialized financial products (e.g., fixed income credit, discounted credit rights) may experience occasional delays or require additional verification due to differing data structures and maturity levels.

- Systematic solutions: The Association’s governance framework facilitates the identification of operational gaps and coordinated implementation of technical and procedural improvements across participating institutions. This replaces fragmented, institution-by-institution problem-solving with a more unified and standardized approach.

Looking Forward: A Model for Global Reference

The developments shared in the country’s latest Open Finance report mark Brazil’s shift from purely regulatory oversight by the Central Bank to a co-governed model led jointly with the Open Finance Association. This transition has strengthened performance, coordination, and trust across the ecosystem. By balancing investments in innovation, security, and governance, Brazil has built a scalable framework that is now attracting global attention.

For Brazilian customers and institutions, this governance model ensures that the substantial public and private investments of recent years continue to enhance accessibility, reliability, and innovation in financial services. The structure established under Resolution BCB 400/2024 provides stability for long-term growth while maintaining flexibility to adapt to new technologies and market dynamics. As a result, Brazil’s Open Finance stands as one of the most advanced and sustainable models of digital financial transformation worldwide.